- Insights

Why the intermediary is the way forward for trusted and compliant digital identity

ㅣ

Maïlys Mas

Digital identity is no longer a vision. It is here. Europe is leading with eIDAS 2.0, which will take effect in just a few months. From the European Digital Identity Wallet (EUDIW) to Aadhaar in India and mobile driver’s licenses (mDL) in the United States, billions of people are moving their identity into smartphones.

This shift promises instant access and convenience, and it is already underway:

India: more than 1.4 billion people use Aadhaar daily.

Europe: the EUDI Wallet rollout is mandated by eIDAS 2.0, with adoption expected to reach 80% by 2030.

United States: 143 million people projected to use mobile driver’s licenses by 2030.

Africa: countries like Nigeria and Kenya expanding national digital ID programs.

By 2029, more than 1.5 billion people worldwide will rely on digital identity every day (Goode Intelligence).

For businesses, the question is not if digital identity will arrive, but how to connect to it securely and compliantly. Today’s infrastructure is fragmented, costly, and prone to fraud. What’s missing is the equivalent of a grid for identity: a trusted layer that ensures each interaction is legitimate, secure, and compliant. That role is the intermediary.

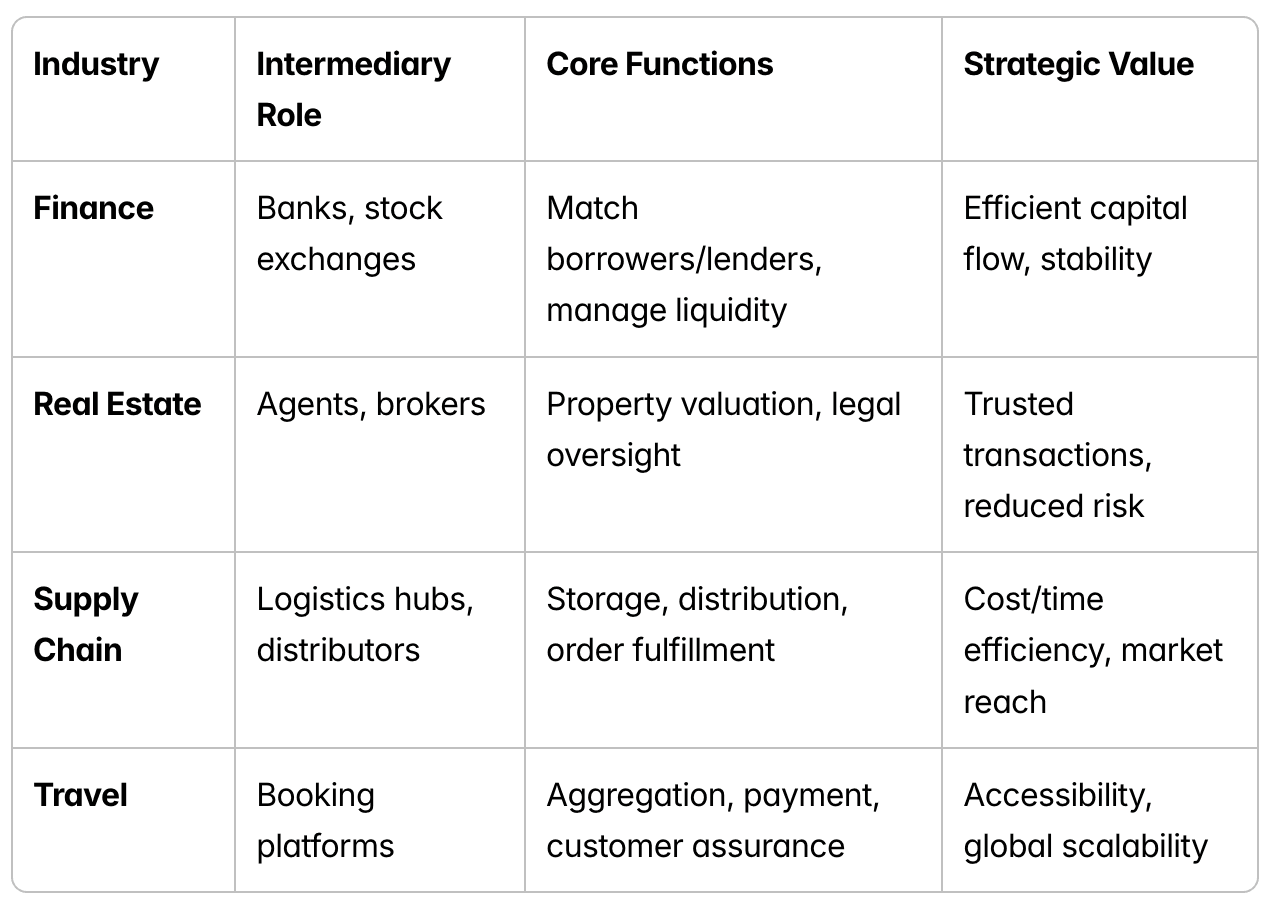

Intermediaries: A proven concept in every industry

Intermediaries are not new. They exist wherever complexity must be managed and trust must be enforced. Finance, real estate, logistics, and travel all rely on them. Without intermediaries, these industries would collapse into inefficiency.

Identity has reached the same point of maturity. It now requires its own intermediary role.

The digital identity ecosystem today, and what’s missing

The digital identity ecosystem has strong foundations:

Issuers: Governments and private bodies create eIDs

Wallets: Citizens hold and use their credentials

Relying parties: Businesses need to verify customers

IDV providers: Use traditional methods such as document checks and biometrics to verify identity

Brokers/aggregators: Connect issuers, wallets, and relying parties by relaying data, but don't guarantee the full chain

IDV providers and brokers have limits in the world of eIDs and wallets. IDVs rely on traditional methods like document checks and biometrics. Brokers act like pipes: passing information along without necessarily verifying and validating each step of the process. At a global scale it creates risks, engineering debts, and compliance failures.

Digital identity needs more than connection. It needs validation and assurance. That’s where intermediaries come in.

What is an intermediary in identity

The eIDAS 2.0 Architecture and Reference Framework (ARF) defines intermediaries as a special class of relying party. They are neutral actors that request attributes from wallets on behalf of businesses, verify the authenticity and status of credentials, and immediately delete the data after use.

eIDAS 2.0 Architecture Reference Framework — 3.11 Relying Parties and intermediaries

In practice, this makes intermediaries the trust layer of digital identity. Unlike brokers or relays that only transmit, intermediaries validate every action in the chain: confirming issuers, verifying holders, and ensuring relying parties are authorized. Each interaction is signed, timestamped, and auditable.

Intermediaries are to identity what Visa and Mastercard are to payments

Banks issue cards, cardholders use them, and merchants accept them. But the system only works because a neutral network like Visa or Mastercard sits in the middle: verifying, routing, and securing each transaction without holding the funds themselves.

Intermediaries in identity play the same role:

Issuers create credentials

Holders present them

Relying Parties need to verify and accept them

Intermediaries are the neutral trust layer that validates every exchange, without storing the data

It’s what makes the whole system usable and secure at scale.

Why intermediaries matter for companies

For businesses, intermediaries are not a future luxury, they are a present necessity:

Every relying party request is verified

Every user action is cryptographically signed and timestamped

Data is returned both normalized for business use and as original credential data with evidence for audits

Compliance is enforced automatically through standards (e.g., ACR/AMR values to retrieve the Level of Assurance)

In short: intermediaries transform digital identity from isolated connections into a verifiable, compliant, and auditable framework. For companies in regulated industries, this means fewer risks, faster onboarding, and compliance readiness for the future.

Hopae Connect: The trusted intermediary for digital identity

Hopae Connect — following its partnership with INCERT GIE — is aiming to become a pioneer intermediary service in Europe. In other words Hopae Connect is becoming the identity grid of the digital economy. It doesn’t replace issuers, wallets, or relying parties, but it adds the missing assurance layer.

Every action, whether initiated by a relying party or approved by a holder, is validated. The relying party is checked, the user’s credentials is verified, their consent is cryptographically signed, and the exchange is timestamped. Nothing is stored, but everything is secured.

What enterprises gain with Hopae Connect

Global coverage: accept 100+ eIDs and wallets across Europe, the U.S., LATAM, and Asia

Data normalization: tones of eID formats unified into a single schema

Level of Assurance enforcement: compliance with eIDAS 2.0, AML, and GDPR built in

Credential validation: Hopae Connect decodes the credential response and verifies its status with the Trust Registry

Evidence integrity: Hopae returns both the normalized data (for business use) and the original credential data with evidence, so relying parties can trust and audit every exchange

Conclusion: The shift to intermediaries is inevitable

By 2029, billions will rely on digital identity every day. Without intermediaries, businesses face fragmented integrations, rising fraud risks, and compliance exposure.

Every other industry already relies on intermediaries to scale and build trust. Now, digital identity has one too.

Hopae Connect is that intermediary

Learn more about how it can secure and scale your eID integration!

Or request a demo today.